Cloudism Library Stack on Blockchain Archives and Library Futures

Despite a global shift toward the digital, ranging from cultural production to economic exchange, the art world remains decidedly oriented to what is essentially a pre-industrial system: one wherein value is tied to material objects, and transfers of property preferably happen face to face.

Increasingly, however, the cloud is playing host to recognized works of new art, as well as to new and more comprehensive forms of digital legal tender capable of certifying author- and ownership within a single transaction. Here, Library Stack (a living collection of independent digital art media) examines the emerging blockchain ecosystem, considering how, within it, art and financial currency – which are both, after all, speculative containers for value – can and will be differentiated.

1.

In the spring of 2015, MAK (Museum for Applied Arts) Vienna announced that they had used the popular cryptocurrency Bitcoin to acquire a work of art: “Event Listeners,” an animated screensaver by the artist Harm van den Dorpel. The work was made available for sale through the virtual gallery Cointemporary, also based in Vienna, which sells limited-edition digital artworks exclusively with Bitcoin. More than just a financial exchange tool, Bitcoin is used by Cointemporary to record the authorship, sales, and ownership data that authenticate each work. The gallery does this by partnering with the Berlin-based firm Ascribe.io, which enables artists and galleries to securely store the identifying information and full transaction history of any digital artwork (from a text file to a complex bundle of code) as a package of metadata on Bitcoin’s blockchain (a redundantly distributed and cryptographically secured transaction ledger). The metadata is linked to the work upon registration by a unique cryptographic signature, or hash, by which the work can then be traced anywhere across the web.

A digital file’s typical registration on Ascribe will include its title, author, technical metadata, the initial upload timestamp (which can back future intellectual property claims), and the file’s newly minted hash, a unique alphanumeric string. Because Bitcoin’s blockchain is duplicated across numerous individual computers and is maintained through strictly outlined forms of participatory consensus, it is often termed “trustless,” in that it claims to not need the oversight of a government or bank to authenticate its transactions. By providing certificates of authenticity backed by the credibility of this technology, Ascribe allows ownership of digital assets to be reliably proved, and thus later sold, auctioned, or transferred. Since the 1960s, authenticity certificates have been used to relocate the value of a dematerialized or conceptual work into a legally validated paper surrogate so that it can participate in the money economy, a gesture borrowed from commodities markets. Hashing a file is the digital version of this: the data-embedded concept is inexorably tethered to the metadata that proves its identity, enabling it to be valuable in a commodity system. Any new buyer of a work registered on Ascribe can verify the object’s entire metadata history by looking up the hash and inspecting the blockchain. Ascribe’s services translate the art market’s existing sales and provenance paradigms into digital space upon firmly established legal foundations.

But all translations are imperfect. Galleries have recently been struggling to find a clear basis for value between a digital work’s natural liquidity and the prized legacy mandates of physical singularity, authenticity, and scarcity. Many have imposed clumsy constraints, keeping edition numbers artificially low and contractually turning servers, computers, or other contingent hardware into surrogates for the soft works they contain, ignoring the implication that new protocols for valuation, ownership, and exchange might be necessary. The production expenses of these digital works (including their software, data storage, transmission, computational time, and access to the internet) are either negligible or presumed to be figured within other costs of business. These works use no degradable paper, ink, paint, chemistry, magnetic tape, or plastics, and they are infinitely duplicable without quality loss (“perfectly durable” in legal terms). As even more new artworks take non-material form (e.g., serial apps, archival databases, unplayable video games, synthetic narratives in VR space), traditional efforts to control their relationship between circulation and value will become even less effective, further strengthening the draw of blockchain verification.

But while using Ascribe replicates the surface effects of object ownership, it doesn’t articulate an immanent logic for digital value. Ascribe does not distinguish, for example, between an original file and its duplicate, only between rightful and unrightful (read: legal or illegal) possession. The hash of a given file always copies and pastes with that file, so any duplicate still produces the same ownership metadata when checked against the ledger. A copy would just prove that the correct file had found its way into the “wrong” hands. Since it is unfeasible for an owned digital artwork to be actually unique, Ascribe enables it to be functionally unique: if the work can be reliably identified by its specific owner, the external legal regime can enforce the circulation control. This process heralds the arrival in fine art of what has already taken hold across music, film, and literature: a shift in commodity valuation from an object’s intrinsic objective properties to its extrinsic intellectual ones, or from material authenticity to legal authorization.

Harm van den Dorpel, “Event Listeners,” 2015, screen shots

Harm van den Dorpel, “Event Listeners,” 2015, screen shots

2.

Cryptocurrency itself might be digital art’s closest analog for a norm of valuation. Within their own ecosystems, cryptocurrencies like Bitcoin or Ether (the currency of the blockchain platform Ethereum) relate computational demand to energy supply: their token value is premised on the electricity, data storage, and processing power needed to “mine” them (that is, crunching advanced cryptographic math problems and being rewarded with tokens upon success), in addition to whatever artificial scarcity was initially imposed by the platform’s creators. These currencies facilitate tasks and services on their respective platforms, but their dollar value exchange rate only reflects the beliefs and enthusiasms of their users. Like cryptocurrency tokens, digital artworks are simply data bundles that are only valuable in particular exchange contexts. Both are types of stored value assets, pressured by the contradictory demand of remaining scarce while being liquid. Both punt the question of their own value into the future.

Coincident with Conceptualism’s reformulation of art’s material terms and social purview came one of the more innovative attempts to parse (and provide some control over) its commodity value. Seth Siegelaub’s “The Artist’s Reserved Rights Transfer and Sale Agreement” (1971) was a sales contract template for artists, bundled with a healthy dose of career advice. It maintained that art was a special category of commodity, unlike any other, with a floating valuation outside the complete control of either artist or collector. The agreement claimed that a work’s value depended on the subsequent successes and continued creative labor of the artist – essentially, that the value of a given work is a function of its author’s social capital – and maneuvered the legal system to reinforce the mutuality of the artist-collector relationship. It is easy to imagine that the enforcement possibilities offered by a blockchain-based system would give Siegelaub’s contract renewed traction for today’s artists. But the patronage relationship between “known” artist and “known” collector was central to that document. In today’s era of avatars, handles, and online personae, it would seem that both have already begun their disappearance.

Cointemporary still seems optimistic about the market to come, though. They write that Bitcoin represents a “new form of autonomy in the global monetary system, which does not yet exist in a similar fashion in the art world.” Setting aside the novelty of this ostensible autonomy, it is true that blockchains and cryptocurrencies are making inroads into the fine art market where other post-internet technology trends (like online auctions, social networking, or direct sales platforms) have failed to live up to investor expectations. This is because, again, a blockchain can certify both authorship – which is still the principal logic of value allocation in the fine arts – and the chain of ownership, which undergirds the secondary market. And yet, a blockchain can also help solidify existing forms of digital anonymity. As hash keys on compressed files come to replace artists’ signatures, authorial identity will be occluded by mathematical randomness: the touch of the artist will be registered in the QR code. At the same time, any buyer in an online marketplace can be cloaked by an alias account or generic email. Thus, a work’s provenance might soon become only a chain of anonymous (or pseudonymous) market transactions, its value eaten away by the very technology that claims to credibly certify it. The unaccountable social metrics of art’s valuation will bend toward the pixelated certainty of blockchain protocol. This signposts a larger paradox: proof of ownership without proof of identity; accurate public sales records without buyers. Crypto-transparency will be the cultural logic of distributed autonomy.

3.

Blockchain publishing services also target a broader scope of commercial graphic artists and freelance creatives. One such example is Po.et (“an authentication and certification platform”), which offers a free hashing system that allows creatives to inscribe independent digital files with usage terms, copyright data, royalty rates, and permission restrictions before that given file enters general circulation on the web. Po.et duplicates each data-heavy file into a distributed BitTorrent library, and stores the lightweight metadata of the file’s hash on the Bitcoin blockchain. The work can always be found by whomever might want to buy it, and the conditions of that sale, determined by the artist upon initial registration, are forever baked into the work. The Po.et hash is less a provenance ledger than a licensing ledger; on this platform, the commodity always carries the exchange mechanism within itself. Offering the free hashing service incentivizes more artists and designers to index their work in Po.et’s ecosystem. But the company ambitiously plans to use this growing pool of material as the basis for becoming a large, distributed media clearing-house for select corporate buyers, with safely pre-licensed content and frictionless legal frameworks. Currently in its initial “Rosetta” phase, Po.et will pass through a second stage, “Gutenburg,” on the way to “Alexandria,” at which point it will operate a broad commercial content archive entirely of its own making and licensing.

From language to book to library : Po.et knows that the real power is in owning the distribution network rather than the individual low-value contents that flow through it. Po.et is a marketized archive produced in advance, and while it offers artists and creators the ability to bind their intentions to the work they make, those works must always live in Po.et’s ecosystem, subject to its corporate marketplace and the legal regime that supports it – which, by definition, conceives of ownership as a form of authorized licensing. While creators are presumably free to register their files elsewhere under different terms, the Po.et-hashed file’s circulation outside the network is proscribed, and any usage not explicitly enunciated is disallowed by default. The nature of registering a proof-of-existence timestamp means the artist must outline a work’s permissions “upon entry,” and so be able to conceive and define all possible future uses at the moment of the work’s birth. But how could one know what a work will someday need, who will need it, what they’ll want to do with it, and on what technical platform? Aspects of this scenario are already visible with Amazon or Apple’s proprietary walled gardens: by participating in their distribution network, artists yield to the platform’s “click-wrap” contract restricting their e-books or objects from entering public library collections, academic lending, or civic institutions. Public is here construed in a zero-sum relationship to the private: while the work is widely distributed commercially, it is kept invisible from the public record.

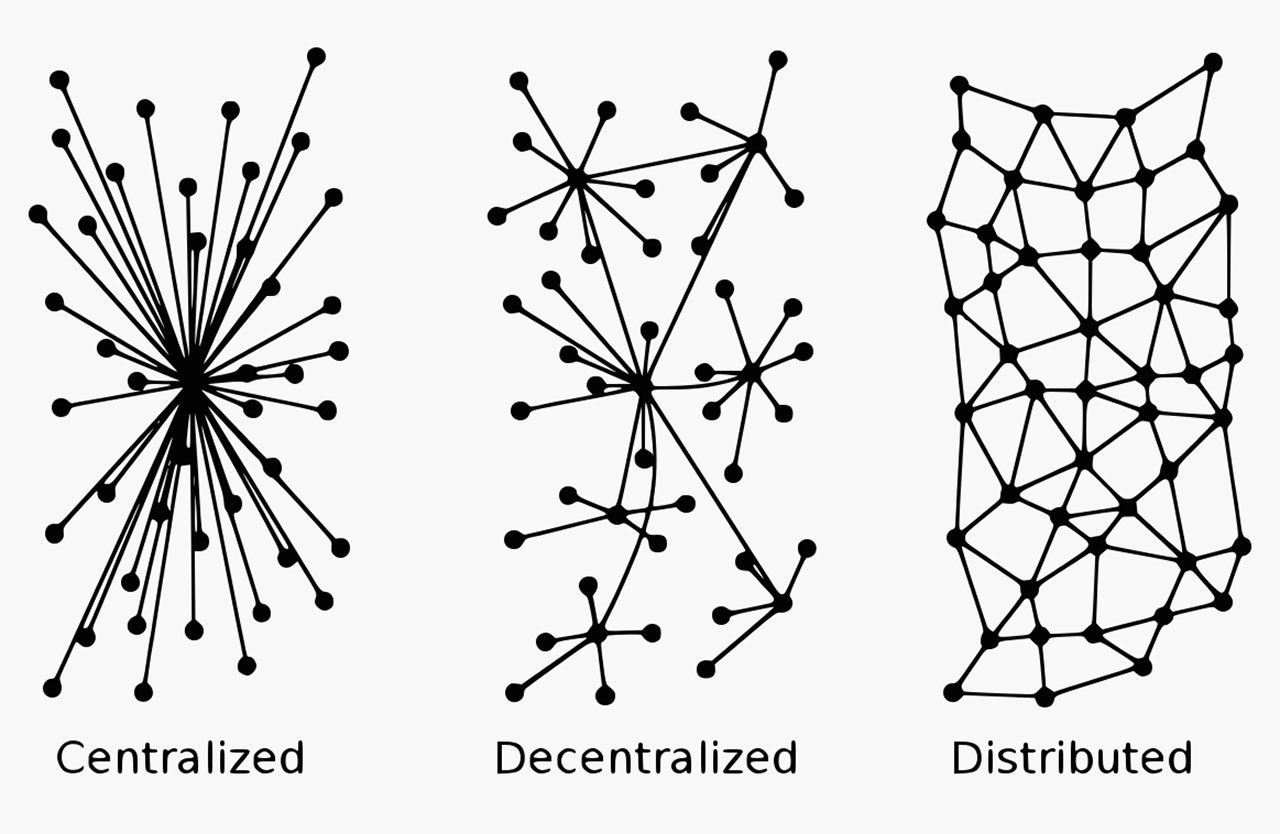

Network configurations (Paul Baran, RAND, 1964)

Network configurations (Paul Baran, RAND, 1964)

4.

The common material of digital media – streams of binary data – has already engendered a technical and formal convergence of artwork, software, and publication with a formal hybridity that subsumes legacy media distinctions. The podcast-as-artwork, exhibition-as-.zip folder, artwork-as-code bundle, and the serial PDF journal are now recognizable forms of publication, just as the archive-publisher, self-assembling library, or downloadable radio station are platforms for content. Convergence of form will produce a corresponding convergence of program, and another of ownership. Already, artwork and publication are clearly only rhetorical frames indexing a digital file’s intended valence of distribution along a shared continuum of readers, users, and enthusiasts. When an artist is commissioned to make an app, is that app a digital artwork, or is it just an app? If that artist already has an established career or reputation, then which museum department should be responsible for collecting it? How should it be described in the catalogue, displayed to the visitor, interacted with, or contextualized? Irrespective of these works’ low cost and capacity for infinite reproduction, their cultural currency is finite: either they are immediately important within a particular sphere of artistic production or they lay dormant until some unknowable moment when they might explode into relevance. This notion of cultural finitude charts value as a function of social potentiality: it is an index of a work’s own ability to exceed its artist’s expectations or intentions, a value that must sit outside of monetization. Catalyzing or manifesting a work’s degree of cultural finitude requires it being circulated, read, experienced, and used by a wide public. Librarians and archivists, likewise prompted to reorient towards futurity, might see collecting digital artworks as a form of speculation on their cultural value. This is all the more urgent since blockchain verification of digital artworks presupposes its ownership enforcement through intellectual property law, as is already the case with music, books, and films. If there is a functional digital equivalent of aura , it is currently being hemmed in as a commercial feature.

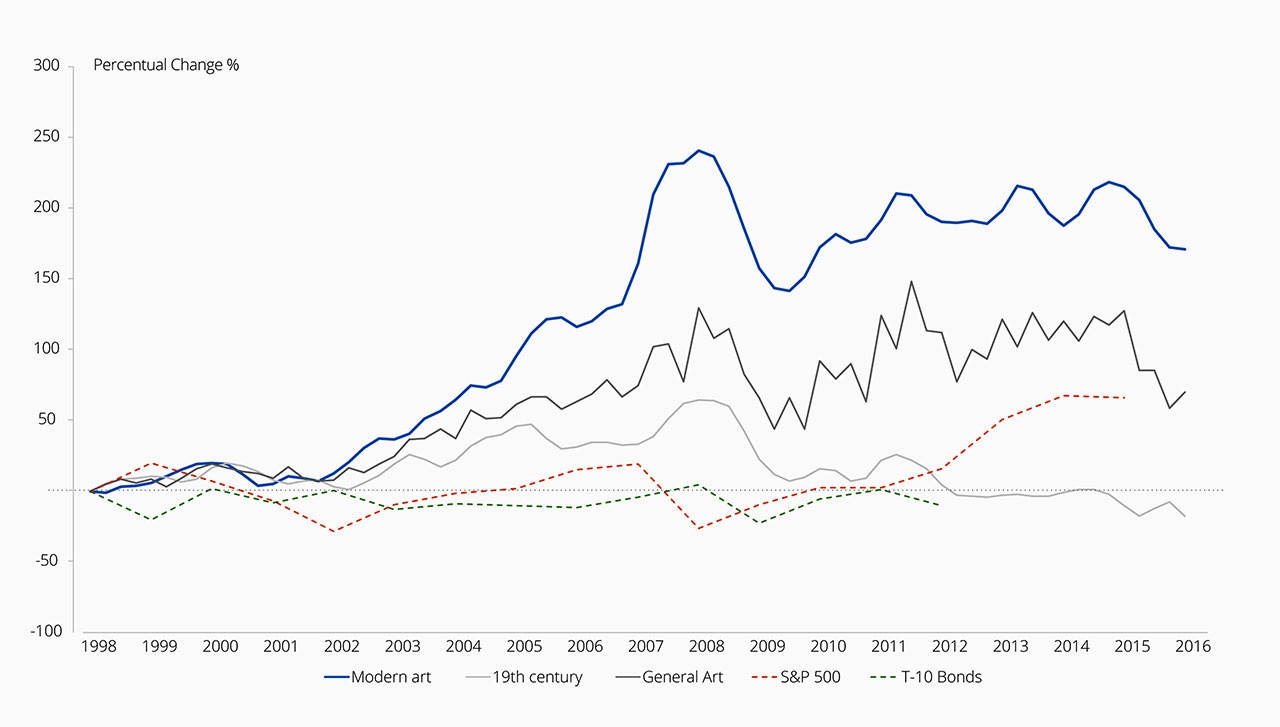

Market performance of fine art compared to other asset classes 1998-2016 (via Maecenas.co)

5.

Owning a material artwork like a sculpture or a painting without the cultural mandate or social reward for doing so is an unattractive investment proposition. They are illiquid, demanding, fragile, temperature-sensitive objects that are highly taxed and expensive to store, insure, and transport. The financial payoff from auction or resale can take forever. Yet total annual global art sales are estimated at some $65 billion, with roughly another $3 trillion sitting in storage. The online art marketplace Maecenas, a platform built on the Ethereum blockchain, allows for a new market in the stored values of these material artworks by legally distilling them into distinct quantities – similar to issuing shares in a company – and securely hashing them for individual sale within the Maecenas ecosystem. When a work is brought to auction on the platform, fractions of its ownership might change hands multiple times, and competition among the widened pool of possible owners drives up the value of the work. The object itself need never leave the freeport. Maecenas already envisions even further markets in derivative financial products, all backed by the value of the stored artworks within its system. This mechanization of fine art value follows the general automation of derivatives markets into formulas and algorithms, and instantiates the core dream of all blockchain technologies: defrictionalizing the movement of money, as the web has already done with information. As meta-ledgers, blockchains are able to record any cascading chain of transactions irrespective of geographic, material, or political stakes. They enable trading markets even in things that have never before been commodities: ontological concepts, ephemeral human capacities, cartographic coordinates, or the presumed future values of cult objects in storage. Any abstraction can be made convertible into money via the cryptocurrency of each idiosyncratic trading platform designed for precisely that notional market. Blockchain liquifies even the most stubbornly material of values.

While Maecenas calls itself the first “decentralized art gallery,” it is more accurately described as a trading market in art-values or art-futures. In “The Specter of Capital” (2014), Josef Vogl describes how markets seek to efface future volatility by using risk-offsetting investments and by exploiting future risk. Yet, if all terms were known, there would be no speculative value. Capital dreams that it can know the future, but inevitable quotients of unknowability are the differentials upon which profit accrues. It is this demand to minimize the gap between the unknowable future and the notion of futurity itself that drives this detethering of art value from art object. Marketization and derivation both increase value and accelerate the pace of payoff. After all, profit on the future value of an artwork must take place in the future; but profit on art-futures can take place right now, in the present.

6.

Given ecological crisis, material scarcity, and the energy consumption of the global technology stack, cultural finitude (simply the unknowable horizon into which any artwork is cast) might be more useful as a rubric for decoding the present than as an abstraction about the future. Artists must ask themselves, “Is this object worth making?” just as archivists must ask, “Is this object worth saving?” Using a new platform called Augur.net, one can now even ask more precisely: “What art objects will the future need?” Built on the Ethereum blockchain, Augur is a platform for prediction markets: atomized, local betting rings on the future likelihood of real-world events. Individual users pose core questions and finance the setup costs of a market that takes predictions on only that question, profiting from other users’ participation irrespective of the ultimate outcome. The cost of a single tradeable share correlates to the root question’s probable likelihood, and fluctuates as the subject nears its real-life resolution date. The notion that a purely unregulated market will derive an accurate assessment of future outcomes by distilling the aggregated beliefs of its actors (the wisdom of the crowd conceit) is beloved by Libertarian-leaning economists. But by keeping a perfect record of a futures market in the value of predictions, Augur is blockchain’s conceptual feedback loop (or perhaps its inner daemon run amok), construing the market as a machine that can answer the questions of its own actors. While others see simple exchange values mediating fundamentally unknowable questions, or at best a cryptographically secured casino, Augur sells the belief in well-aligned innards. It wants security from an unknown future and yet locates all value there. Like other Silicon Valley blockchain startups, its kitsch atavism for the ancient past only indexes the degree to which it aims to lock down the potentialities of the future. As with any good oracle, you can ask Augur about anything: coming ecological disasters, political assassinations, economic bubbles, basketball tournaments, or art’s potential for cultural transformation. Presumably, at least a few of the anonymous bettors soon to use Augur’s platform will be curious artists, thinkers, curators, or archivists, wagering on future potentials and the cultural finitude of their own urgent questions.

- Title image: Harm van den Dorpel, “Event Listeners,” 2015, installation view

Library Stack is an archive and publisher focusing on digital art objects, co-edited by Benjamin Tiven and Erik Wysocan. https://www.librarystack.org and https://twitter.com/lbrystk